The scale up of STRC and SATA has drawn in many detractors.

Recently Onramp published a paper highlighting some issues of Digital Credit. There were some errors and the paper was clearly AI-generated in most places. My favorite error actually had little to do with Digital Credit, and it appeared in the preface of the report (imagine you haven’t even started reading the actual paper and you already see a factual error, this is the level of AI we are dealing with).

Onramp writes on Page 3: “Strategy has released AI-generated advertising featuring a young, attractive model in a tropical setting”

But a quick viewing of the 30-second ad they are referencing shows that the woman worked “hard as an engineer”, not a model. This is literally 10 seconds into the ad, which is about the same amount of time it took me to spot the error in Onramp’s preface.

I just thought this anecdote was funny. Onto my main point.

Their core argument was that Digital Credit could be better replicated by combining U.S. treasury securities with BTC. (This is what Onramp calls “the simpler trade” but I also fail to see how this is simpler considering that buying digital credit involves just one single ticker while “the simpler trade” involves a dynamic re-laddering of maturing treasury bonds combined with BTC held on a separate venue.)

This conclusion is wrong. It is trivial to show that it is wrong empirically (one just has to look at the daily returns time series of Digital Credit instruments vs a portfolio of IBIT and SGOV or IEF). But this missive will present multiple economic arguments for why we can know a priori that the claim is incorrect.

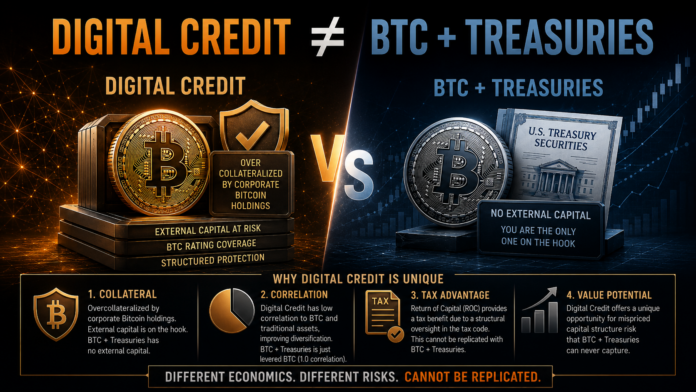

Reason 1: Collateral

Digital Credit is overcollateralized by corporate bitcoin holdings. This cannot be replicated with one’s own equity because there is no committed external capital in the case of owning BTC and treasuries—it is all your own money and no one else is on the hook. Credit is different. Even though the principal is yours, there is external capital in the form of the issuer’s assets that are committed to ensuring you are made whole. This capital is “external” because it existed before you ever put your principal in and it remains well after you sell your position.

To be precise, an unencumbered bitcoin balance sheet isn’t collateral in the strict sense, but it serves as collateral in a flexible sense. For instance, a BTC-backed loan with margin call is collateralized in a strict sense because the collateral is set apart for the debt. Digital Credit gives the issuer more flexibility with collateral management, but it also gives the investor more flexibility because the security is fungible and liquid. This is an understanding that both parties agree to.

The presence of the collateral is protection for the investor. This coverage is expressed in the BTC Rating metric, which is the ratio of Bitcoin NAV to the sum of the notional value of a particular credit series and all more senior series.

A portfolio of BTC and treasuries has no external capital. This fact alone makes it impossible to economically replicate what is going on in Digital Credit with BTC and treasuries.

Before I move on, I should address treasuries. It is true these are backed by the full faith and credit of the Federal government, and this might be considered a type of collateral. Some might even call this infinite collateral coverage. However this implicitly assumes that the U.S. will not default on its debt. Onramp mentions that because the government can print money and it is constitutionally illegal to not pay the debt, the treasuries position is therefore a sure thing.

This does not account for a case where the government revises its policy and defaults on some debts but not others. Such a move should not be deemed impossible considering the growing influence of modern monetary theory, which posits that sovereign debt is a mere construct constrained only by inflation. MMT sees debt as a reallocation of society’s resources across time to generate the highest social benefit in the present. This line of thought is really the final destination of fiat finance where everything is relative and based on high time preference decision-making.

But under this logic, a move to “delete” the debt owed to some parties while honoring the debt owed to others would, assuming the parties are selected correctly, constitute a partial debt jubilee that would still allow currency stability to persist. Is the treasuries risk worth taking? Everyone must decide for themselves. If this does happen, then STRC will be fine (since the dollar would be fine, because we already said that currency stability persists) but the treasuries and BTC portfolio could see some heavy losses.

Combining BTC with treasuries therefore introduces that avenue for risk which Digital Credit, being a fully structured overcollateralized bitcoin position, does not have.

In other words, the real difference between Digital Credit and a synthetic replication is the type of risk that the investor endures. Keep this point in mind, because it is a recurring theme.

Reason 2: Correlation

Markowitz portfolio theory shows diversification as the only free lunch in finance. When multiple uncorrelated things are stacked together, they can create higher risk adjusted returns.

Digital Credit is rather uncorrelated to bitcoin and other assets. STRC is at 0.63 correlation to BTC and 0.33 correlation to SPY and a 0.33 correlation to the S&P preferred stock index.

Like everything else, it is true that it can be positively correlated during times of high stress. But the lower correlation most of the time means that Digital Credit can improve the diversification of portfolios.

In contrast, it is easy to show that bitcoin and treasuries cannot do this because it is simply a watered-down bitcoin position: bitcoin levered by some number between 0 and 1. For example, 20% BTC and 80% treasuries is really just 0.2x levered BTC. 0.2x levered BTC still has a 1.0 correlation with BTC, so it offers zero diversification benefits to a larger portfolio that already holds BTC. In finance jargon, we might say that this has a 0.2 beta but a 1.0 correlation.

The reason Digital Credit can generate lower correlation is precisely because of the capital structure behind it. The company has many different options that are unavailable to the investor that holds only BTC and treasuries. These options create idiosyncratic factors that are independent from and therefore uncorrelated with BTC.

And just to reiterate the earlier point, these idiosyncratic factors are also different risks that the Digital Credit investor accepts.

Reason 3: Tax

This is probably the biggest error from Onramp. Return of Capital is a tax benefit in the case of STRC and SATA. Onramp argues that it isn’t a benefit because the company has no earnings and so the capital really is return of principal and therefore economically similar to the return of principal in their laddered treasuries model. While this is true for many cases of ROC, it is not the case for Digital Credit.

First, understand that the ROC tax rule for negative taxable earnings and profits was designed with the assumption that companies would make their money via fiat-denominated cash flows rather than taking advantage of the fiat’s debasement to accumulate appreciating assets.

For just a moment, I want you to seriously consider why a distribution from a company without earnings would be a reduction of cost basis. Why is this rule fair and why did it come about?

The answer is that a company that doesn’t have income but pays a distribution is economically liquidating itself, which means the principal (cost basis) of all equity investors should be reduced to reflect this partial liquidation. In most cases of ROC, the entity gets smaller as the distributions occur, because the distribution was literally part of the entity. You can see this for yourself in covered call ETFs that go through brutal NAV erosion while paying out ROC distributions.

But again, this whole dynamic assumes as a premise that companies only make money with cash flows and not by investing in appreciating assets. If in fact there existed a company that could make money by investing in appreciating assets, then it could easily take advantage of the ROC tax rule by making it look like it was partially liquidating while in reality growing larger and larger.

And if you look closely, this is exactly what Strategy is doing. Its enterprise value gets larger as it pays out more ROC distributions. This is completely the opposite of what one would expect to see with ROC when thinking from first principles, or what one actually sees in other ROC cases. When BTC starts to rally, this difference gets even clearer.

This distinction alone should make it clear that Digital Credit offers something very unique. It has ROC, which we may think of as an accounting treatment of principal erosion, without the economic reality of principal erosion being reflected by a lower share price. This is, in short, a structural arbitrage made possible by an oversight in the tax code (the oversight being that C-Corps do not make money by holding appreciating assets). This is unique to Digital Credit and cannot be replicated by BTC and treasuries.

But just like Digital Credit today benefits from this tax rule, it could also stop benefiting should the rule change. We should expect a reprice of Digital Credit in that kind of event. This is a risk that Digital Credit investors accept, and it is a risk that the BTC and treasuries portfolio does not have.

Reason 4: Value Investing

Value investing is about buying undervalued assets. Assets are undervalued when the market does not assess the risk correctly. It is possible that the risk associated with the corporate structure is not priced correctly, and therefore the Digital Credit investor earns a higher risk premium than what is justified. This could explain the double digit yields on Digital Credit instruments.

Therefore, getting a potential bargain is another benefit. It is of course true that treasuries might be a bargain. And it is of course true that BTC is a bargain. But it is also undeniable that neither can ever express the unique bargain of a misunderstood capital structure, which is what Digital Credit offers.

Conclusion

Finally, it is fair for an investor to believe that the risks of Digital Credit are not worth it. However, this would not be the point of the article, which is to demonstrate that Digital Credit offers at least four unique benefits that a BTC and treasuries portfolio cannot replicate.

The claim that such a portfolio can better replicate digital credit is false because such a portfolio does not at all replicate the underlying economics of Digital Credit.

The benefits of Digital Credit derive from a different set of risks inherent to the unique capital structure of a Bitcoin treasury company. Therefore the economic facts prove that Digital Credit cannot be replicated without a similar capital structure.